Audit RFPs are among the most scrutinized documents in professional services. Buying committees. They’re typically led by the CFO and composed of board members, independent directors, and procurement stakeholders who evaluate audit proposals across regulatory depth, commercial understanding, and operational reliability.

With invitation-to-tender windows opening 12 to 18 months before the audit period, the proposal itself is often the final differentiator between similarly qualified firms.

This guide covers every component of a high-performing audit proposal: executive summaries that address RFP requirements directly, scope sections structured for complex engagements, compliance frameworks tailored to industry regulations, and pricing strategies that maintain auditor independence.

Key takeaways

- Audit proposals require a tailored approach and can benefit from proposal creation tools for sleek, responsive designs.

- Different types of audits require different information in the proposal, highlighting the need for separate audit proposal templates for each audit type.

- Building relationships with the Audit Committee at the target account can increase chances of receiving an audit RFP.

- A well-structured audit proposal includes key sections like executive summary, scope of audit services, compliance requirements, project timeline, qualifications, fees, and specific RFP requirements.

- Qwilr's audit proposal template provides a professional, customizable format for creating audit proposals that potential clients can review and sign without leaving the document.

What is an audit proposal?

An audit proposal is a formal document submitted by a licensed audit firm, including regional CPA firms and Big Four practices, to a prospective client in response to a Request for Proposal (RFP). Audit proposals present a structured offer of audit services across a defined engagement scope and help organizations meet regulatory and market standards.

The audit process covers two main types: internal and external audits. External audits satisfy obligations to outside parties like government agencies, regulatory bodies, and shareholders and are subject to strict auditing standards, including GAAP, PCAOB, and SEC reporting requirements. Internal audits are discretionary, governed by the company itself, and can be conducted by employees or outsourced to independent auditors.

| Audit Type | Primary Purpose |

|---|---|

Financial statement audit | Verify the accuracy of financial records for stakeholders and regulators |

Tax audit | Review tax filings for compliance with federal and state requirements |

Global audit | Assess finances and operations across multiple countries or jurisdictions |

Employee benefit plan audit | Evaluate compliance of retirement and benefit plans (e.g., ERISA requirements) |

Compliance audit | Confirm adherence to industry-specific regulations |

Payroll audit | Verify payroll accuracy and tax withholding |

Information systems audit | Assess IT controls, cybersecurity, and data integrity |

Operational audit | Evaluate the efficiency and effectiveness of core business operations |

The audit type determines which credentials, regulatory requirements, and team expertise to lead with in your proposal. A global audit engagement, for example, requires demonstrated experience in cross-border regulatory frameworks — something the Audit Committee will verify against competitors on the shortlist. A second global audit consideration is jurisdiction-specific compliance, which should be addressed explicitly in the scope section.

An auditor provides several different kinds of audit services, so it makes sense to increase sales productivity with a separate audit proposal template for each kind of audit they offer clients.

Why audit bids matter

Audit committees evaluating competing firms will draw conclusions about working relationship quality from the proposal itself before a single meeting takes place.

Beyond the engagement mechanics, audit services serve a broader organizational function for businesses:

- Financial health: Audits provide an independent view of an organization's financial position, identifying problems before they become crises

- Stakeholder trust: A credible, well-structured audit proposal signals to shareholders, board members, and regulators that the organization takes its compliance obligations seriously.

- Strategic insight: Audit findings inform leadership decisions on risk, capital allocation, and long-term planning: well beyond the annual compliance sign-off

- Reputational standing: Organizations that engage rigorous, qualified auditors demonstrate accountability to regulators and external parties

A proposal that clearly communicates this value, including the firm's commitment to providing excellent service, positions the audit firm as a strategic partner from the start. For potential clients comparing firms, that impression often carries as much weight as credentials.

How to increase your chances of receiving an audit RFP

Audit tenders at larger organizations are typically public knowledge 12 to 18 months before the audit period. That window gives audit firms time to build relationships with Audit Committee members like the CFO, who generally serves as the primary point of contact throughout the engagement.

Firms that win competitive tenders consistently do three things before delivering the audit RFP:

- Map the full Audit Committee structure at target accounts through sales prospecting and identify not just the CFO but also independent directors, legal counsel, and procurement stakeholders

- Establish credibility through relevant touchpoints like industry events, thought leadership, and direct outreach to committee members

- Research the client's industry, regulatory requirements, and prior audit history so the proposal reflects a genuine understanding of their situation and helps define the right scope from the outset.

Audit firms that treat pre-RFP relationship-building as a structured sales process with defined touchpoints, assigned contacts, and tracked interactions consistently outperform firms that rely on reactive outreach.

A note on nonprofit audit RFPs

Nonprofit organizations have specific audit requirements that standard RFP templates rarely account for, particularly around grant compliance and restricted fund reporting.

Before issuing an RFP, nonprofit boards and audit committees should:

- Align internally on audit priorities before the RFP goes out — grants, restricted funds, and any recent regulatory changes should all be on the table

- Have a financial expert review the RFP before sending it to confirm that the scope and compliance requirements are accurately described

- Ask peer organizations and trusted contacts for firm recommendations rather than relying solely on open tender processes

Nonprofits receiving federal grants are subject to Uniform Guidance (2 CFR Part 200), which imposes audit requirements that a generic template will not cover. Tailoring the audit RFP to the organization's specific fund structure and disclosing any related items, such as restricted funds or grant compliance obligations, produces more relevant, comparable proposals from responding audit firms.

Key components of a winning audit service proposal

A strong audit proposal follows a clear structure that addresses every audit RFP requirement while guiding the Audit Committee through the firm's approach, qualifications, and fees without overwhelming the reader.

The sections below cover each core component, from the executive summary through to the conclusion. Each one serves a specific purpose in building the committee's confidence that the audit firm understands their business, their regulatory environment, and that the engagement team will deliver on time and within scope.

Executive summary

The executive summary gives the Audit Committee a focused overview of how the audit proposal addresses their RFP requirements through the firm's methodology, relevant industry expertise, and engagement approach.

Audit proposals that lead with the firm's strongest differentiators give the Audit Committee immediate context for everything that follows. This is where differentiating evidence belongs:

- Industry-specific credentials and certifications

- Prior engagements of comparable scope and complexity

- AICPA peer review results

- Proprietary methodologies that competitors are unlikely to replicate

Keep the argument tight. Senior stakeholders outside the finance team, like board members, legal counsel, and executive leadership, frequently have limited time to review full tender documents or engage in lengthy sales conversations. The executive summary is their primary contact point, and a strong one can define the entire audit firm's positioning before a single meeting takes place.

Scope of services

The scope of audit services defines exactly what the engagement and your audit approach cover:

- Specific financial statements under review, and whether consolidated or standalone reporting applies

- Draft financial statements and related documentation

- Internal controls testing

- Regulatory compliance deliverables

- Any additional items specified in the audit RFP

- Risk assessment methodology

- Resources the audit firm will commit, like team size, seniority mix, and any specialist resources required for complex regulatory areas

Specificity matters here since vague scope definitions create room for misalignment on deliverables, which erodes trust with clients before the engagement begins.

This section carries significant technical weight. Proposal software like Qwilr allows firms to organize complex scope details using interactive pricing tables and collapsible content sections, keeping granular information accessible without overwhelming the reader.

The scope section should also show a commercial understanding of the client's business like the regulatory requirements they face, the complexity of their company structure, and how the engagement team plans to address both.

Where confidential information is involved, the proposal should define how the audit firm will handle, store, and disclose it in line with applicable standards.

Compliance and regulatory requirements

The compliance and regulatory section outlines how the engagement satisfies compliance obligations at the federal, state, and local levels. Requirements vary by client type:

| Client Type | Key Compliance Requirements |

|---|---|

Publicly traded companies | SOX, PCAOB, SEC reporting rules |

Non-profits (federal grant recipients) | Uniform Guidance (2 CFR Part 200) |

Healthcare organizations | HIPAA, CMS audit standards |

Financial services firms | FINRA, Basel III, state banking regulations |

Government contractors | FAR, DCAA audit requirements |

Also specify which auditing standards govern the engagement, like GAAS for financial statement audits, GAGAS for government engagements, or PCAOB standards for public company work.

Where the client's audit RFP has outlined specific compliance obligations, address them directly and in the same order they appear. This makes it straightforward for the Audit Committee to verify they haven’t missed anything across all regulatory requirements.

Lastly, explain materiality thresholds, including how testing levels are set and why, transparently rather than left to assumption.

Project timeline

The project timeline maps every activity and deliverable against the audit period, anchored to the board meeting date at which the audit firm presents final results.

Map each phase backward from the board meeting date to ensure project completion aligns with filing deadlines and management review windows. Include:

- Fieldwork and on-site visits

- Draft financial statements

- Management review periods

- Regulatory filing deadlines

- Final sign-off and board presentation

- Client responsibilities

Each milestone should specify which party is responsible — engagement team or client — so accountability and responsibility are clear from day one.

Client document delivery directly affects timeline integrity. Building response windows and late-delivery contingencies, including any late fee provisions, into the timeline gives the Audit Committee a realistic picture of how the engagement runs and supports the timely delivery of final financial statements.

Qualifications and experience

The qualifications section shows that the engagement team has expertise specific to the client's industry, entity type, and regulatory environment.

Relevant credentials to include:

- CPA and CIA certifications

- Specialist designations (e.g., CISA for information systems audits)

- Prior engagements of comparable scope and complexity

- AICPA peer review results

- Industry verticals covered: healthcare, financial services, government contracting, non-profit

Note: Where engagement team members have a financial background directly relevant to the client's industry, like healthcare finance, government contracting, or nonprofit fund accounting, mention that experience explicitly. Listing the auditing standards the firm is licensed to work under gives the Audit Committee immediate confirmation that the engagement team meets the baseline requirements for the engagement type, too.

Beyond credentials, Audit Committees are evaluating working relationship fit — whether the audit process will be organized, communicative, and manageable for the finance team running it day to day. Where key personnel on the engagement team have direct experience with the client's industry or entity type, name them and connect their background explicitly to the scope.

Costs and fees

Audit engagement fees are primarily driven by scope: hours required, team seniority, and entity complexity.

Fee structures typically account for:

- Fieldwork hours broken down by seniority level

- Document turnaround time where client responsiveness directly affects billable hours

- Compliance complexity where additional regulatory requirements add scope

- Late-delivery provisions that include clearly defined windows to protect both parties

Fee proposals that break down costs by audit phase, such as planning, fieldwork, review, and reporting, give the Audit Committee a clearer picture of where time is being spent and why. Where pricing flexibility exists, audit firms can incentivize efficient client engagement. Engagements where clients deliver requested documents promptly require fewer hours to complete, which can reduce fees meaningfully.

Auditor independence rules impose strict limits on cross-selling within audit engagements. Any non-audit services must be scoped, disclosed, and offered in compliance with PCAOB and SEC independence requirements. Where non-audit contracts are already in place, the proposal should clarify how the audit engagement interacts with those arrangements and disclose any potential independence considerations upfront.

Conclusion

The conclusion is not the place to restate the proposal's argument. By this point, the Audit Committee has reviewed the firm's methodology, qualifications, and fees in full.

Instead, the conclusion should make it straightforward for the client to act and close the deal:

- Terms and conditions: Link directly to T&Cs rather than attaching separate documentation

- Next steps: Define what happens immediately after acceptance: kickoff timeline, primary contact details, and document request process.

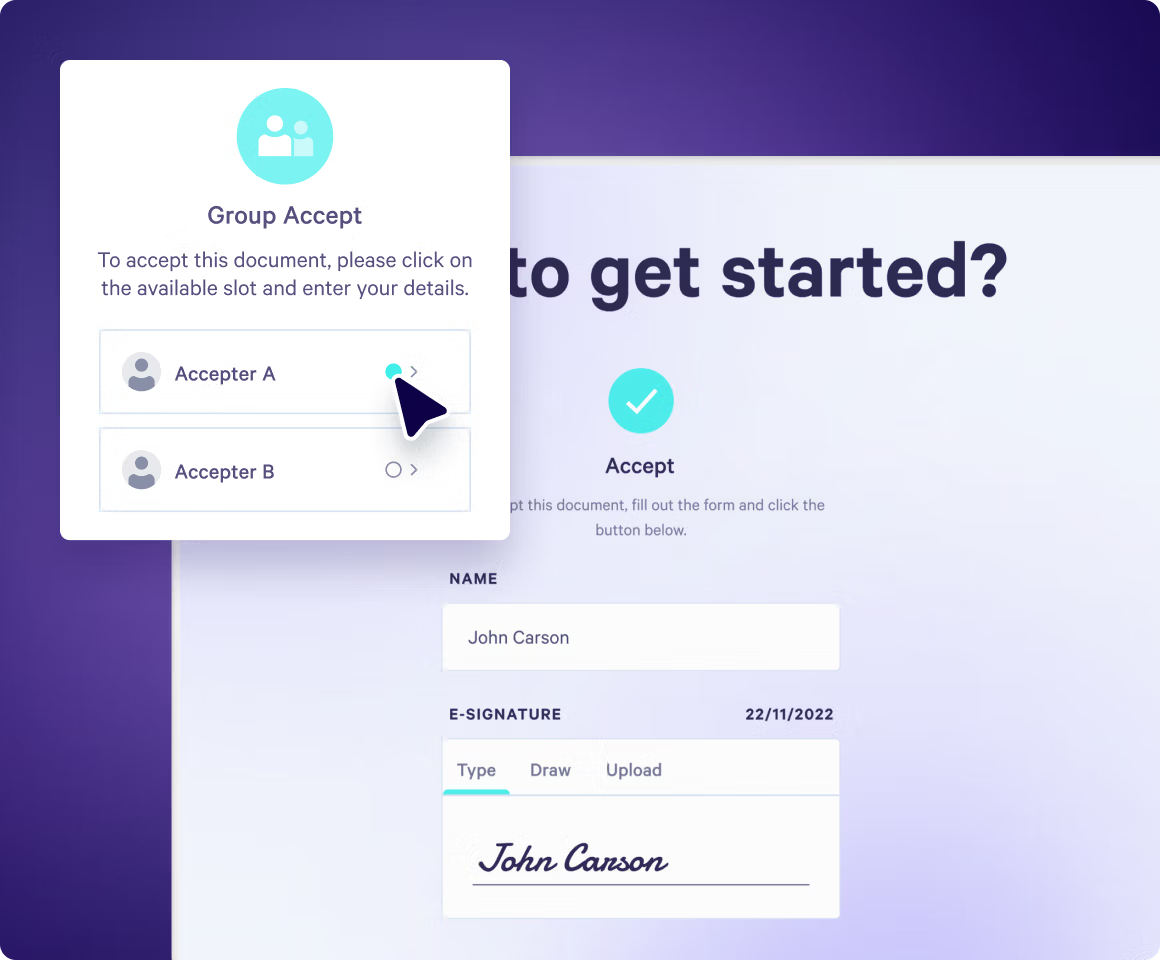

- E-signature functionality: Qwilr proposals include built-in e-signature and contract acceptance, so the Audit Committee can approve the engagement without navigating to a separate platform, streamlining the final step of the audit process.

The kickoff communication also sets expectations for deliverables beyond compliance sign-off, like process improvement recommendations, risk mitigation findings, and management letter items.

For nonprofit organizations in particular, this is where grant compliance reporting responsibilities and restricted fund assurance obligations should be confirmed with all relevant parties.

Example of an audit proposal template

Qwilr’s audit proposal template provides everything you need to deliver a baseline proposal you can differentiate for different clients or types of audit.

Each section of Qwilr's audit proposal template serves a specific purpose:

- Executive summary

- Scope of services

- Compliance and regulatory requirements

- Project timeline

- Qualifications and experience

- Costs and fees

- Specific requirements from the RFP (optional)

- Conclusion

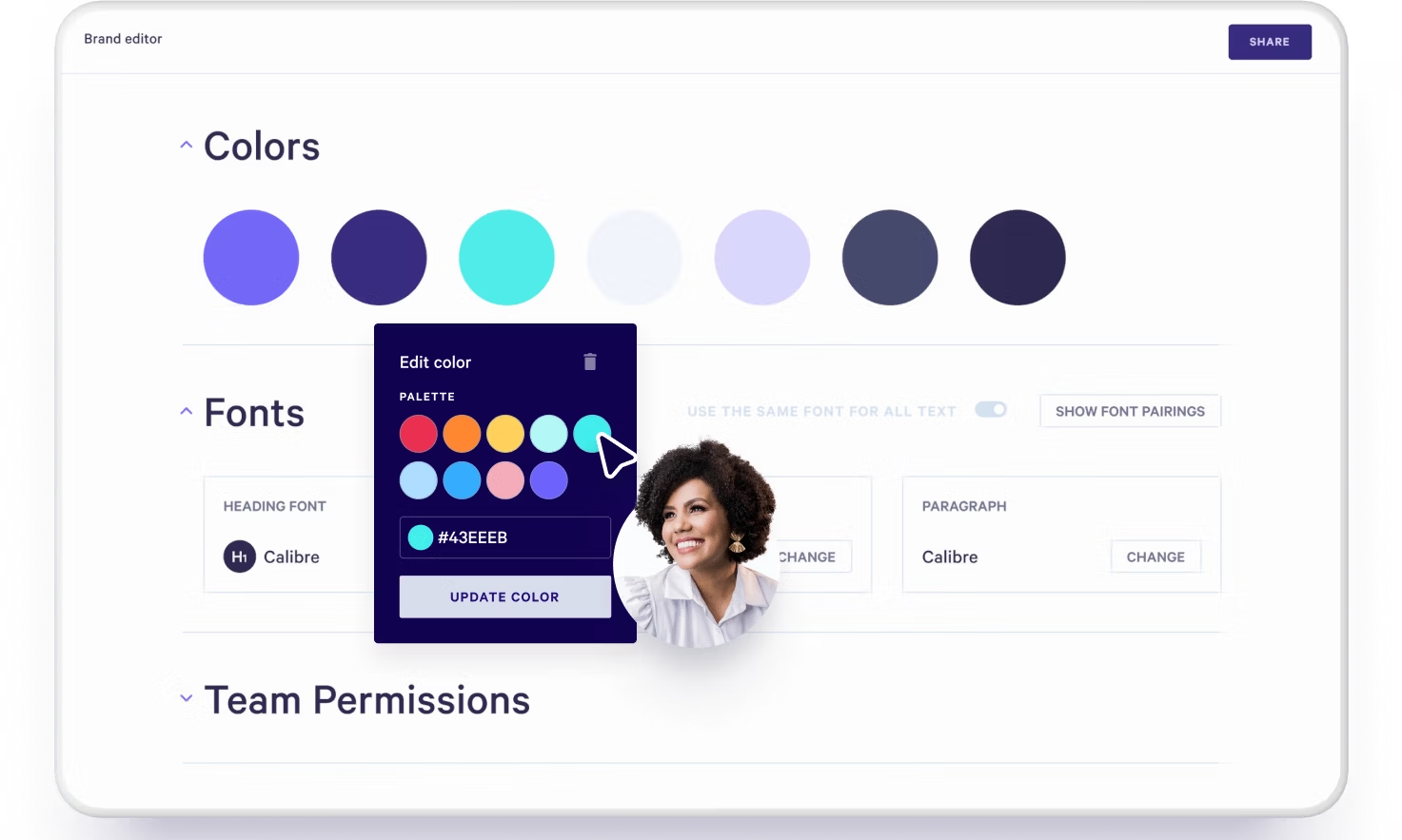

Qwilr proposals are professionally designed and mobile-friendly. They’re instantly adaptable and customizable with any content you want to introduce. Import your branding elements and incorporate interactive elements such as embedded videos, image galleries, and interactive pricing tables for added impact.

Customize proposals to match the changing needs of the audit

Audit proposals rarely come together in a single draft. Scope changes, new compliance requirements, and client-specific details mean the final version often looks very different from the first. Having flexible, well-structured templates means your team spends less time rebuilding from scratch and more time tailoring the details that actually win the work.

Building a library of reusable templates with each mapped to a specific audit type gives your team a faster starting point without sacrificing the specificity that competitive tenders require. Qwilr's 14-day free trial lets you see how much time that saves in practice. Give it a shot today.

About the author

Kiran Shahid|Content Marketing Strategist

Kiran is a content marketing strategist with over nine years of experience creating research-driven content for B2B SaaS companies like HubSpot, Sprout Social, and Zapier. Her expertise in SEO, in-depth research, and data analysis allow her to create thought leadership for topics like AI, sales, productivity, content marketing, and ecommerce. When not writing, you can find her trying new foods and booking her next travel adventure."

Frequently asked questions

An effective audit proposal should open with a stand-alone executive summary. The document created should also outline the following:

the scope of the audit program

the auditor’s qualifications and experience

compliance and regulatory requirements

the project timeline, costs, and fees

A comprehensive internal audit should look to establish a baseline for each of the four C’s - culture, competitiveness, compliance, and cybersecurity.

A request for proposal (RFP) is a document sent by a company to prospective auditors to help them create a sales proposal that reflects the company’s needs. It contains details about the type of audit required, the organizational structure, and the current operational and financial status of the company.